BLOG

How to File Form 1040NR: A Step-by-Step Guide for Nonresident Aliens

Filing taxes in the U.S. as a nonresident alien can feel overwhelming, but it doesn’t have to be. If you earned income while in the United States and aren’t a

Filing taxes in the U.S. as a nonresident alien can feel overwhelming, but it doesn’t have to be. If you earned income while in the United States and aren’t a

Understanding Section 7E: A Comprehensive Guide to Deemed Income Taxation in Pakistan In this article, we delve into the interaction with Section 7E, a notable addition to the tax laws in

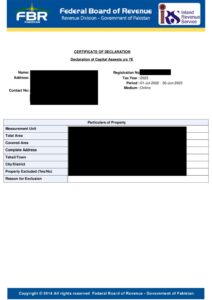

If you’re in Pakistan and need to get your hands on your 7E Certificate from Iris, don’t worry, it’s not as complicated as it sounds. This certificate is super important,

Taxation laws can often be complex and convoluted, especially when understanding the taxation of Conveyance Provided by Employer as outlined in Section 13 Rule 5 of the Income Tax Ordinance

If you’re a Non-US Resident with a Single-Member LLC, you need to file Form 5472 and Form 1120 every year Taxation For Single Member LLC as a Non-Resident If you’re

The Comprehensive Guide to Create LLC in Wyoming: A Step-by-Step Approach” Introduction Welcome to our comprehensive guide on Create LLC in Wyoming! If you’re considering starting your own business and

Introduction In Pakistan, rental income is subject to taxation, whether it’s earned by an individual, an Association of Persons (AOP), or a company. Understanding the nuances of how Taxation on

IT SECTOR TAXATION IN PAKISTAN 2024 Diving into the intricacies of the Income Tax Ordinance of 2001, we find notable adjustments across various sections IT SECTOR TAXATION IN PAKISTAN 2024:

Introduction In Pakistan, filing your Business Tax Return in FBR Pakistan is a crucial obligation that every business owner must fulfill. Understanding the process and requirements for business tax return

Introduction Extension of Time for Furnishing Returns Are you aware of the provisions regarding Understanding the Extension of Time for Furnishing Returns under Section 119 of the tax laws? In